When you swipe your credit card at a shop or pay online using your card, the process feels instant and seamless. You tap, enter your PIN, and the payment is done. But behind this simple action lies a complex financial system where multiple parties are involved—and one of the most important elements in this system is the Merchant Discount Rate, commonly known as MDR. While customers rarely notice it, MDR is one of the key ways banks and payment networks earn money from everyday transactions.

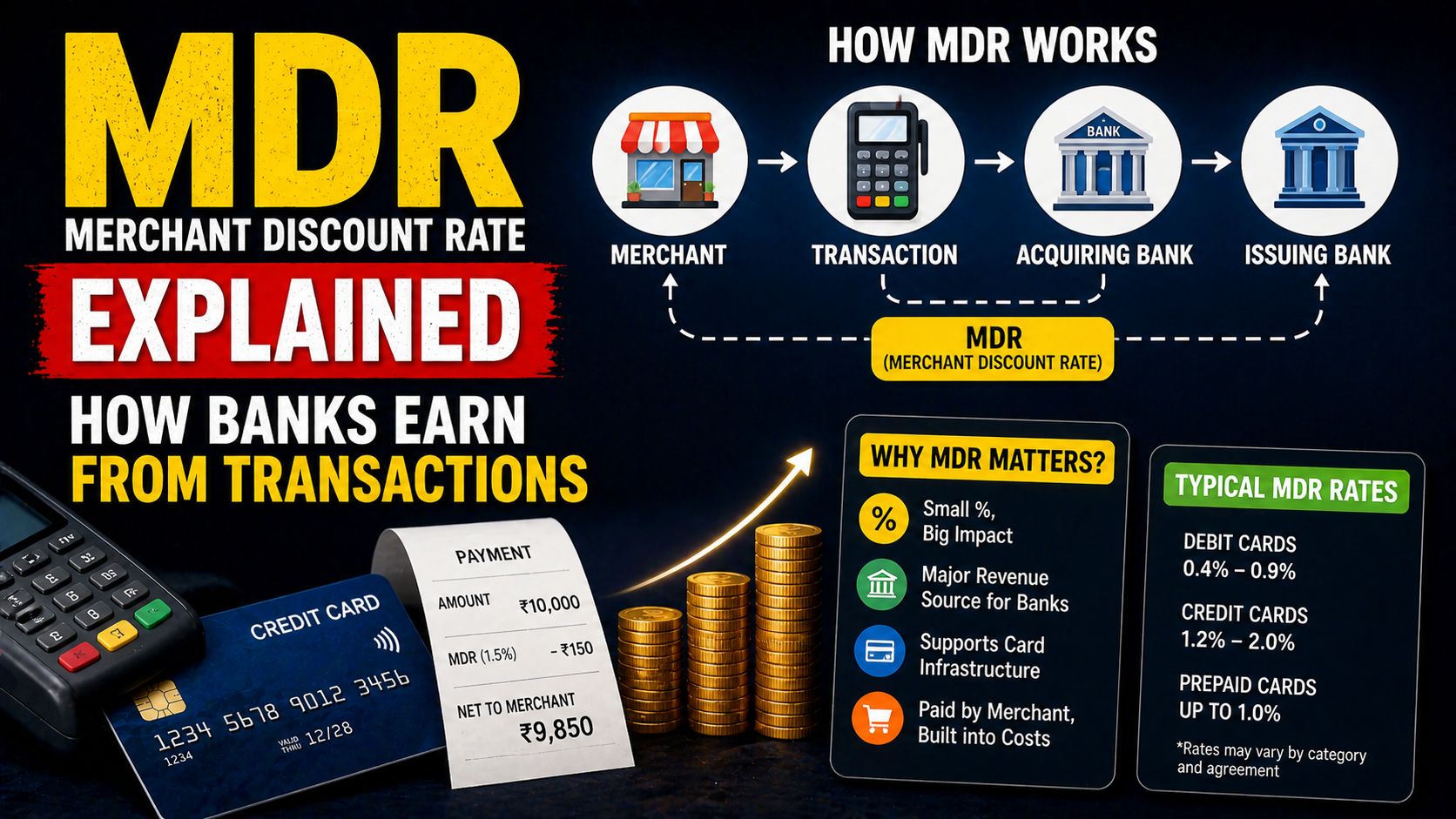

To understand MDR in simple terms, think of it as a small fee that merchants pay every time they accept a card payment. Whenever you make a purchase using your credit card, the shop owner does not receive the full amount instantly. A small percentage of the transaction value is deducted as MDR, and the remaining amount is credited to the merchant’s account. This fee is shared among different players in the payment ecosystem, including the bank that issued your card, the bank that processes the payment for the merchant, and the card network.

In India, MDR typically ranges between 1% to 3% of the transaction amount for credit cards, although the exact rate can vary depending on factors like the type of card, the merchant category, and the payment method (POS machine, online gateway, or contactless payment). For example, if you make a purchase of ₹1,000 using your credit card, the merchant might receive around ₹970 to ₹990 after the MDR is deducted. The remaining ₹10 to ₹30 is distributed among the involved parties.

The structure of MDR is more layered than it appears. A portion of this fee, called the interchange fee, goes to the issuing bank—the bank that gave you the credit card. This is one of the reasons banks encourage you to use your card frequently. Another portion goes to the acquiring bank, which provides the payment infrastructure to the merchant, such as POS machines or payment gateways. The card network, which facilitates the transaction between banks, also takes a small share. This entire system ensures that every card transaction generates revenue, even if the customer pays their credit card bill in full and avoids interest.

One important thing to understand is that MDR is not directly charged to the customer. You don’t see it as a separate fee on your bill. However, it is indirectly built into the pricing of goods and services. Merchants factor in these costs when setting their prices, which means customers ultimately bear the cost in a subtle way. This is why some small businesses prefer cash payments or offer discounts for non-card transactions—they are trying to avoid paying MDR.

In India, the concept of MDR has also been influenced by government policies aimed at promoting digital payments. For example, certain transactions made using debit cards or specific platforms like UPI have zero MDR for merchants, especially for smaller businesses. This has helped accelerate the adoption of digital payments across the country. However, credit card transactions still usually involve MDR, making them a consistent source of revenue for banks and payment networks.

The role of MDR becomes even more interesting when you consider credit card rewards. The cashback, reward points, and discounts that you receive are often funded partly through the MDR collected from merchants. In simple terms, when you earn rewards on your credit card spending, a portion of that benefit is indirectly coming from the fees paid by merchants. This creates a cycle where higher card usage leads to more MDR, which in turn allows banks to offer more attractive rewards to customers.

Online transactions also follow a similar structure, although the rates and distribution may differ slightly. Payment gateways and aggregators come into play, adding another layer to the MDR system. Whether you are shopping on an e-commerce platform or paying for a subscription service, the underlying mechanism remains the same—each transaction generates a small fee that is shared across the payment ecosystem.

For merchants, MDR is both a cost and a necessity. While it reduces their margins slightly, accepting card payments helps them increase sales, attract more customers, and operate in a cashless environment. For banks and payment companies, MDR is a steady and scalable source of income, especially as digital transactions continue to grow rapidly in India.

From a consumer’s perspective, understanding MDR helps you see the bigger picture of how the credit card system works. Even if you never pay interest or late fees, banks still earn money every time you swipe your card. This explains why they actively promote credit card usage through offers, partnerships, and rewards programs.

In conclusion, Merchant Discount Rate is a fundamental part of the digital payment ecosystem in India. It quietly powers the entire system by ensuring that every transaction generates revenue for banks and payment networks. While it may not be visible to customers, its impact is everywhere—from the rewards you earn to the pricing strategies of merchants. The next time you make a card payment, remember that behind that simple tap lies a well-structured system where MDR plays a crucial role in keeping everything running smoothly.

🔥 Related Posts

Buy Now Pay Later vs Credit Cards – Which is Better? (India Guide 2026)

Comparing Credit Card Interest Rates: Which One is Right for You in 2024?

Credit Card Safety Tips for 2024: Protecting Your Digital Wallet

Best Low Interest Credit Cards in India (2026 Guide)

Cashback vs Reward Points Credit Cards – Which Should You Choose in 2026?