In recent years, India has seen a massive shift in the way people spend money. Along with traditional credit cards, a new option called Buy Now Pay Later (BNPL) has quickly gained popularity, especially among young users and online shoppers. Both options allow you to purchase now and pay later, but they work very differently behind the scenes. If you’re confused about which one is better, the answer depends on your financial habits, spending style, and long-term goals. Understanding the differences clearly can help you make smarter decisions.

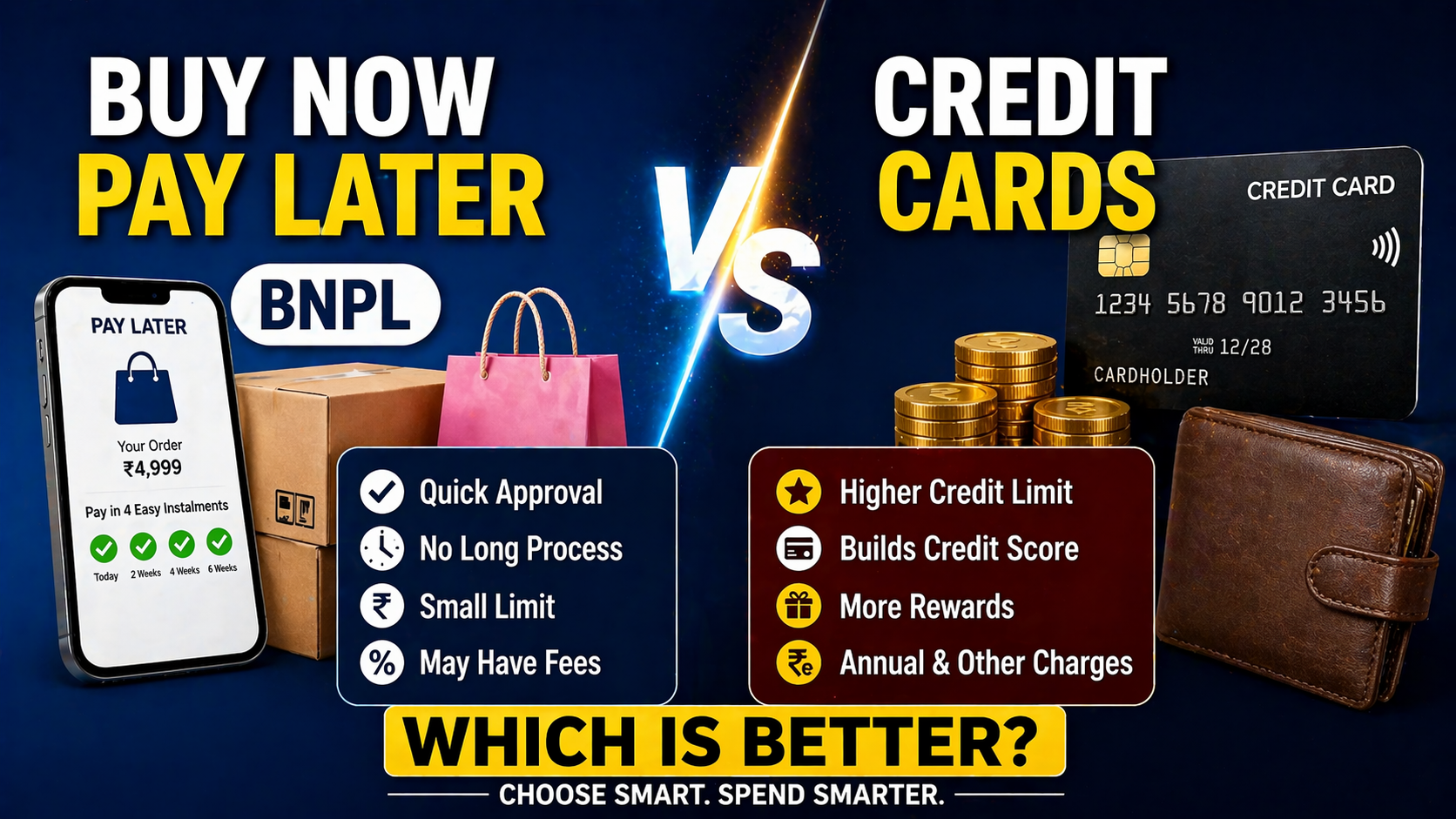

Buy Now Pay Later, as the name suggests, allows you to make purchases instantly and pay for them at a later date, often in small installments or in one go within a short period. These services are usually integrated into e-commerce platforms, making them very easy to use. You don’t always need a high income or a strong credit history to get started, which is why BNPL has become popular among students and first-time earners. On the other hand, credit cards are issued by banks and come with a predefined credit limit. They offer a more structured form of borrowing along with additional benefits like rewards, cashback, and travel perks.

One of the biggest differences between BNPL and credit cards lies in eligibility. Getting a credit card in India typically requires a stable income, a decent credit score, and proper documentation. BNPL services, however, are more flexible. Many providers approve users quickly with minimal checks, making it easier for people with limited credit history to access short-term credit. While this convenience is attractive, it also means users may take on credit without fully understanding the consequences.

When it comes to interest and charges, both options can be either cheap or expensive depending on how you use them. Credit cards offer an interest-free period of up to 45–50 days if you pay your full bill on time. But if you miss the due date or carry forward a balance, interest rates can be quite high. BNPL services often advertise “zero interest” offers, especially for short durations. However, these offers may come with hidden processing fees, late payment penalties, or interest charges if you miss an installment. In both cases, discipline is the key to avoiding extra costs.

Another important factor is flexibility. Credit cards are accepted almost everywhere—online, offline, domestic, and international. You can use them for shopping, bill payments, travel bookings, subscriptions, and more. BNPL, however, is usually limited to specific partner platforms or merchants. While its acceptance is growing in India, it still doesn’t match the universal usability of credit cards.

Rewards and benefits are another area where credit cards clearly stand out. Most credit cards offer cashback, reward points, discounts, airport lounge access, and exclusive deals. Over time, these benefits can add real value to your spending. BNPL services generally do not offer such rewards. Their main appeal is simplicity and convenience rather than long-term benefits.

Your credit score is also affected differently by these two options. Responsible use of a credit card—paying bills on time and maintaining a low balance—can significantly improve your credit score. This helps you qualify for better financial products in the future, such as loans with lower interest rates. BNPL, on the other hand, may or may not be reported to credit bureaus depending on the provider. Some services do report your activity, meaning missed payments can harm your score, while timely payments may help build it. However, the impact is usually less structured compared to credit cards.

Spending behaviour is another crucial aspect to consider. BNPL is designed to make purchases feel easy and frictionless, which can sometimes encourage impulsive buying. Since approvals are quick and repayments are split into smaller chunks, users may lose track of how much they actually owe. Credit cards can also lead to overspending, but they provide monthly statements and clearer tracking, which can help you stay in control if used responsibly.

Security and regulation also differ between the two. Credit cards are issued by regulated banks and come with strong consumer protection features, including fraud protection and dispute resolution. BNPL services, while improving, may not always offer the same level of security or regulatory oversight, especially with newer or less established providers.

So, which is better? The answer depends on your needs. If you are looking for convenience, quick approval, and short-term financing for small purchases, BNPL can be a good option—provided you repay on time. However, if you want a more powerful financial tool that helps build your credit score, offers rewards, and provides long-term value, a credit card is usually the better choice.

In reality, both options can coexist in your financial life if used wisely. You might use BNPL for occasional small purchases on partner platforms and rely on your credit card for regular spending and bigger expenses. The key is not which option you choose, but how responsibly you manage it.

In conclusion, Buy Now Pay Later and credit cards are both designed to offer convenience, but they serve different purposes. BNPL is simple and accessible, making it ideal for beginners, while credit cards are more versatile and rewarding, making them suitable for long-term financial growth. If you focus on disciplined spending and timely repayments, either option can work in your favour. But if misused, both can lead to unnecessary debt. The smarter choice is the one that aligns with your financial habits and future goals.

🔥 Related Posts

Best Credit Cards for Airport Lounge Access in India 2026

Best No-Cost EMI Credit Cards in 2026: Smart Ways to Buy Big Without Interest Burden in India

Best Low Interest Credit Cards in India (2026 Guide)

How Banks Decide Your Credit Card Limit (Internal Algorithms Explained) – India Guide 2026

How to Increase Your Credit Card Limit in 2026 (India Complete Guide)