Credit cards in India are often promoted as “interest-free,” and technically, that’s true—but only if you use them the right way. The moment you don’t pay your full outstanding amount, interest kicks in, and this is where many users get confused. Unlike simple loans, credit card interest is calculated in a slightly complex way, often on a daily basis and compounded over time. If you don’t understand how it works, even a small unpaid amount can quickly turn into a much larger bill. So let’s break it down in a simple, practical way.

To begin with, every credit card comes with an interest rate, usually expressed as a monthly percentage. In India, this typically ranges between 2.5% to 3.5% per month, which translates to around 30% to 45% annually. But banks don’t simply apply this rate once at the end of the month. Instead, they calculate interest daily based on your outstanding balance. This is known as the daily reducing balance method.

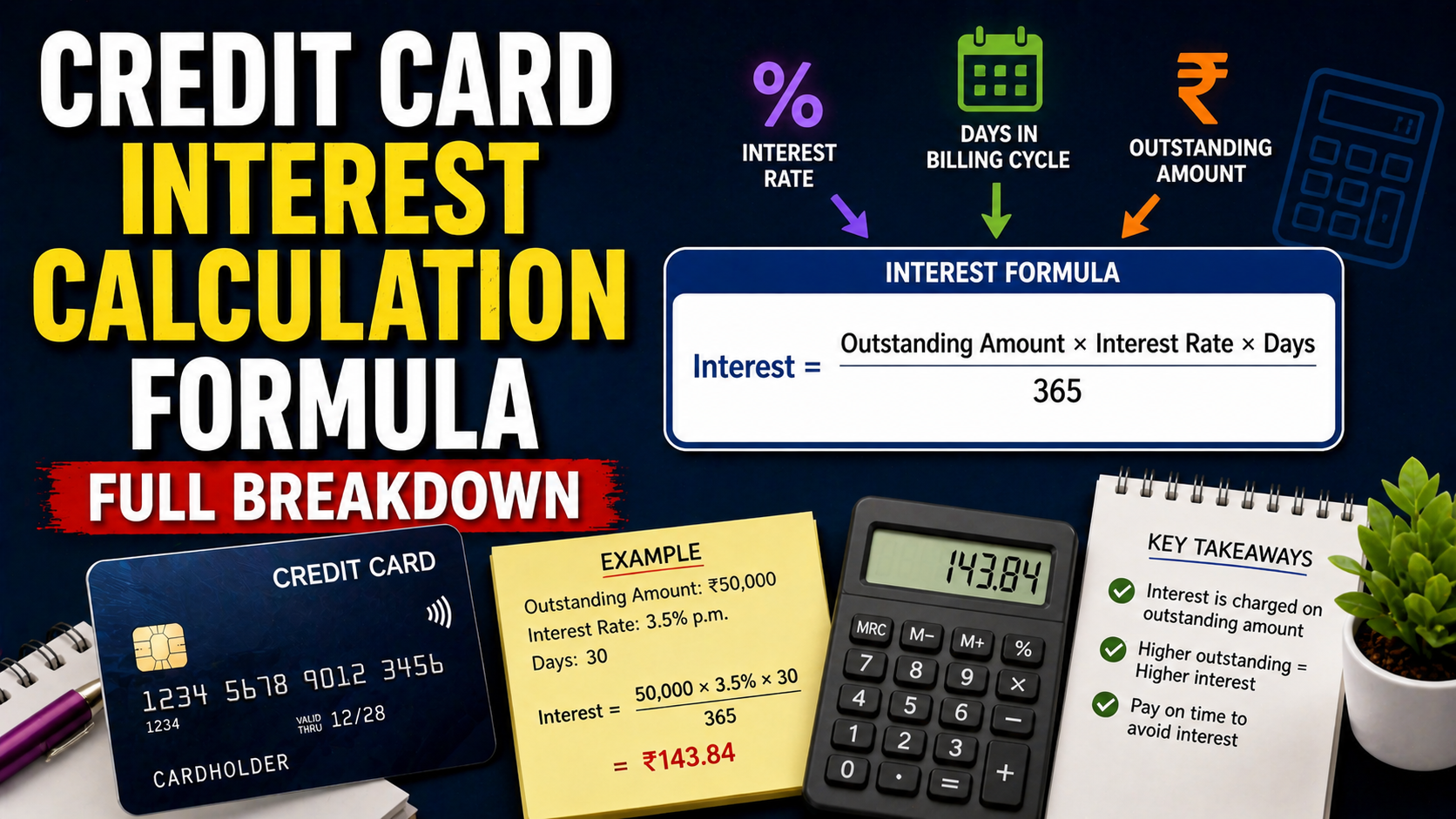

At the core of this system is a simple formula.

Interest = Outstanding Amount × Daily Interest Rate × Number of Days

The daily interest rate is derived from your monthly rate. For example, if your card charges 3% per month, the daily rate would be 3% divided by 30, which comes to 0.1% per day. This may seem small, but when applied every day and compounded, it adds up faster than most people expect.

Let’s understand this with a practical example. Suppose you spent ₹10,000 on your credit card, and your billing cycle ends with a total outstanding of ₹10,000. Now, if you pay the full amount before the due date, you pay zero interest. But if you decide to pay only ₹2,000 and carry forward the remaining ₹8,000, the bank will start charging interest on that ₹8,000.

Assuming a 3% monthly interest rate (0.1% daily), the interest for one day on ₹8,000 would be ₹8. Over 30 days, this becomes roughly ₹240. But here’s the important part—this is just a simplified calculation. In reality, interest is compounded daily, meaning each day’s interest is added to your balance, and the next day’s interest is calculated on the new amount. So the actual interest charged will be slightly higher.

What surprises many users is that once you don’t pay your full bill, the interest-free period is removed. This means the bank may also start charging interest on new purchases from the date of transaction itself. So even if you swipe your card again after the billing cycle, those new transactions may not enjoy the usual grace period until you clear your entire outstanding balance.

Let’s take another example to make this clearer. Imagine you had an outstanding balance of ₹5,000 from last month, and you made a new purchase of ₹3,000 this month. If you haven’t cleared the previous balance in full, interest may be applied on both ₹5,000 and ₹3,000 from their respective transaction dates. This is how many users end up paying much more interest than they expected.

Another factor to consider is the minimum amount due. Your credit card statement usually shows a small minimum payment—often around 5% of the total outstanding. Paying this amount helps you avoid late fees, but it does not stop interest. The remaining balance continues to attract interest daily, which can lead to a cycle of debt if not managed carefully.

There are also additional components like GST, which is charged at 18% on the interest amount and other fees. So if your interest for the month is ₹500, you’ll actually pay ₹590 after adding GST. This further increases the total cost of carrying a balance.

Understanding the timing of your transactions can also help you manage interest better. Purchases made just after the billing cycle starts get the maximum interest-free period, while purchases made just before the cycle ends get the shortest. By planning your spending around your billing cycle and always aiming to pay the full amount, you can completely avoid interest charges.

One of the smartest ways to stay interest-free is to treat your credit card like a debit card. Only spend what you already have in your bank account, and make it a habit to pay your full bill before the due date every single time. Setting up automatic payments or reminders can help ensure you never miss a deadline.

In conclusion, credit card interest in India is calculated using a daily compounding method, which can make even small balances grow quickly if left unpaid. The formula itself is simple, but the real impact comes from how frequently it is applied. The good news is that you can avoid all of it by following one golden rule—always pay your full outstanding amount on time. When used with discipline and awareness, a credit card can remain completely interest-free while still offering all its benefits.

🔥 Related Posts

Mastering Credit Card Tricks in 2026: Smart Hacks to Maximize Cashback, Rewards, Lounge Access, and Savings in India

How to Increase Your Credit Card Limit in 2026 (India Complete Guide)

Buy Now Pay Later vs Credit Cards – Which is Better? (India Guide 2026)

Best Cashback Credit Cards for Online Shopping in India (2026) – Complete Beginner Guide

How Payment Networks Like Visa and Mastercard Actually Work in India 2026