Credit cards are often marketed as a smart and rewarding way to spend money, and in many ways, they truly are. You get cashback, reward points, discounts, and even an interest-free period. But what most people don’t realise—especially first-time users—is that credit cards also come with a range of hidden charges. These charges are not always obvious at the time of applying, and if you’re not careful, they can quietly eat into your savings. Understanding these costs is the difference between using a credit card smartly and falling into a debt trap.

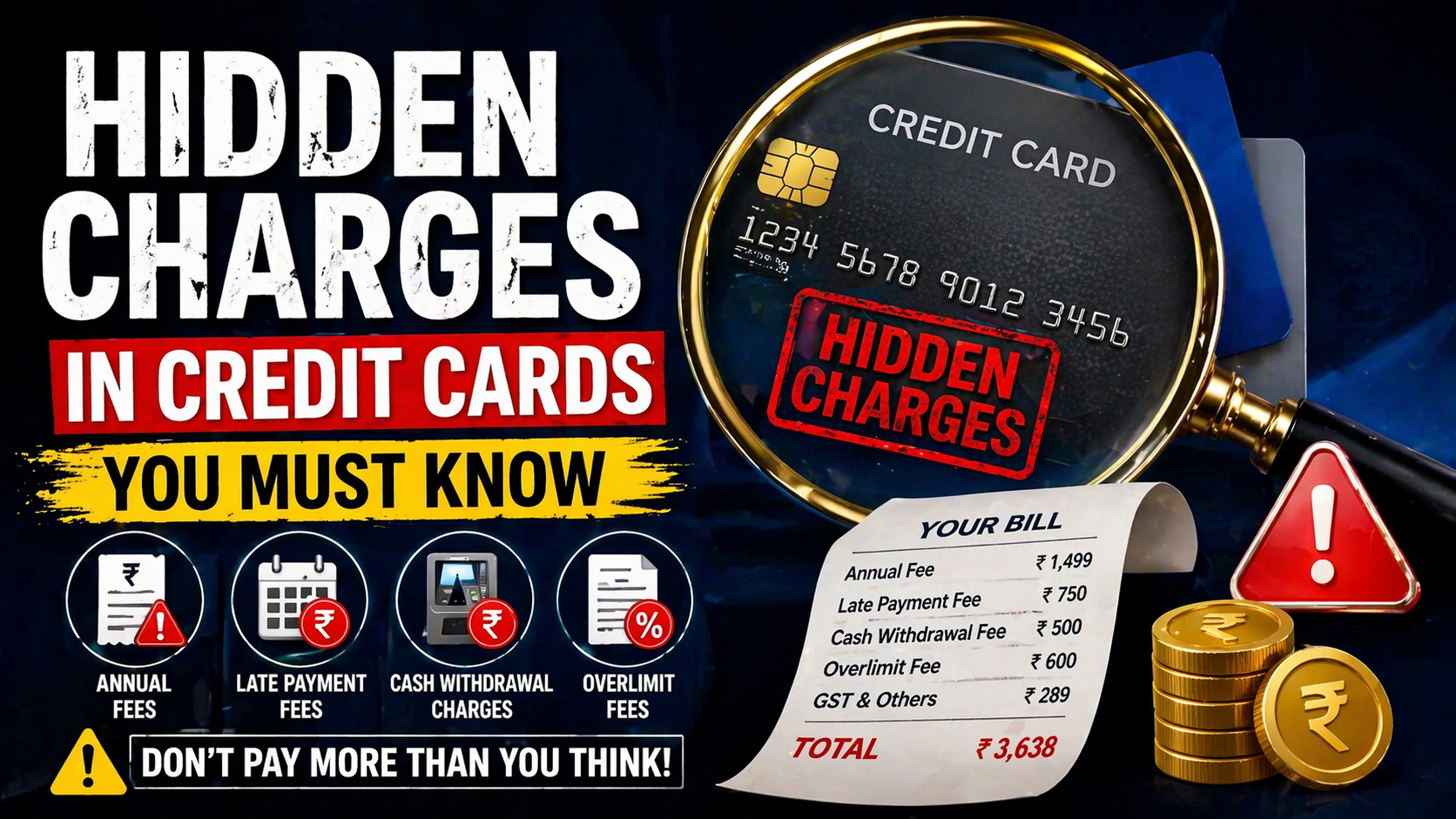

One of the most common hidden costs is the annual fee. Many credit cards in India advertise themselves as “lifetime free,” but that’s not always the full story. Some cards waive the fee only if you meet a minimum spending requirement every year. If you fail to meet that threshold, the fee gets charged automatically. While it may seem small—₹500 or ₹1,000—it adds up over time, especially if you’re not actively using the card.

Another major charge that catches users off guard is the interest rate on outstanding balances. Credit cards in India typically charge anywhere between 30% to 45% annually. What many people don’t realise is that this interest is applied daily if you don’t pay your full outstanding amount. Paying just the minimum due might keep your account active, but it triggers interest not only on the remaining balance but often on new purchases as well. This is where a small unpaid amount can quickly turn into a large bill.

Late payment fees are another cost that’s easy to overlook. If you miss your payment due date—even by a single day—the bank will charge a penalty. This fee can range from ₹200 to ₹1,000 or more, depending on your outstanding amount. On top of that, interest will still be applied, making it a double hit. Consistently missing payments can also damage your credit score, which affects your ability to get loans or better credit cards in the future.

Cash withdrawal charges are among the most expensive features of a credit card, yet many people use them in emergencies without understanding the cost. When you withdraw cash using your credit card, you are charged a fee—usually around 2.5% to 3% of the amount withdrawn, with a minimum charge. More importantly, there is no interest-free period for cash withdrawals. Interest starts accumulating from the very first day, making it a costly option that should be avoided whenever possible.

Another hidden charge that often goes unnoticed is the foreign transaction fee. If you use your credit card for international purchases or even for payments on foreign websites, banks usually charge around 2% to 4% of the transaction amount. This fee is added automatically, and many users only notice it when they check their statement later. If you frequently make international payments, choosing a card with low or zero forex markup can save you a significant amount.

Over-limit charges are also something to watch out for. Every credit card comes with a fixed credit limit, and if you exceed that limit, the bank may allow the transaction but charge a penalty. This fee might not seem significant at first, but it’s completely avoidable with proper spending control. Staying within your credit limit also helps maintain a healthy credit score.

Some charges are even more subtle, like processing fees on EMI conversions. When you convert a big purchase into EMIs, banks often advertise “No Cost EMI.” However, in reality, there may still be processing fees, GST charges, or lost discounts that increase your overall cost. It’s always a good idea to read the fine print before opting for EMI options.

GST (Goods and Services Tax) is another layer that adds to your total cost. Almost all credit card charges—interest, late fees, annual fees, and processing fees—are subject to 18% GST in India. This means every fee you pay is actually higher than it appears at first glance.

There are also charges related to add-on services and subscriptions. For example, if your card offers lounge access, fuel surcharge waivers, or reward redemption options, there might be conditions or hidden fees attached. Reward points themselves can sometimes expire or require a fee for redemption, reducing their actual value.

The best way to avoid these hidden charges is to stay informed and disciplined. Always read the terms and conditions before applying for a card. Keep track of your billing cycle and due dates, and make it a habit to pay your total outstanding amount in full. Avoid unnecessary features like cash withdrawals or impulsive EMI conversions unless absolutely needed. Regularly check your monthly statements to catch any unexpected charges early.

In conclusion, credit cards are not inherently expensive—it’s the lack of awareness that makes them costly. When you understand the hidden charges and how they work, you gain full control over your finances. Used wisely, a credit card can be a powerful tool that offers convenience and rewards without unnecessary costs. But if ignored, those small hidden charges can quietly turn into a big financial burden over time.

🔥 Related Posts

Best No-Cost EMI Credit Cards in 2026: Smart Ways to Buy Big Without Interest Burden in India

How Payment Networks Like Visa and Mastercard Actually Work in India 2026

Best Credit Cards Under ₹500 Annual Fee in India 2026

Best Cashback Credit Cards for Online Shopping in India (2026) – Complete Beginner Guide

How to Apply for a Credit Card in India in 2026: A Complete Step-by-Step Guide with Eligibility, Documents, and Pro Tips